Herbie6590

-

Posts

6082 -

Joined

-

Last visited

-

Days Won

26

Content Type

Profiles

Forums

Uncouth Garb - The BRFCS Store

Everything posted by Herbie6590

-

v Hull City (h) - 31/1/26

Herbie6590 replied to Herbie6590's topic in Blackburn Rovers Fans Messageboard

Did a bit on Radio Lancs on the way home… https://www.bbc.co.uk/sounds/play/m002qfhb?partner=uk.co.bbc&origin=share-mobile -

The January 2026 Transfer Window

Herbie6590 replied to chaddyrovers's topic in Blackburn Rovers Fans Messageboard

It was a little tongue in cheek shall we say…I expected an avalanche of vitriol but perhaps its a sign of how exhausted we all are that I received none…😉 -

Oh yeah…but structure folks expectations 👍

-

There’s not a cat in hell’s chance they’ll discuss this with legal action ongoing…

-

The January 2026 Transfer Window

Herbie6590 replied to chaddyrovers's topic in Blackburn Rovers Fans Messageboard

You clearly haven’t listened to my transfer suggestions on the latest 4000 Holes podcast & I for one am offended…😆 -

The January 2026 Transfer Window

Herbie6590 replied to chaddyrovers's topic in Blackburn Rovers Fans Messageboard

Luca Toni #IYKYK See I’m not the first to suggest this…😆 -

why have they never launched a UK brand would be another good question…

-

When I met with Fraser Reed about kit planning in April 2024 I showed him the Sampdoria section of the Macron website & I said “Do all this stuff…in Rovers colours….” It’s not quite as impressive this season as it was then but still is way beyond what we have ever stocked… https://www.macron.com/en/merchandising/football/clubs/italy/uc-sampdoria.html?p=1

-

https://www.soccerbible.com/interviews/2025/10/diving-into-the-second-season-of-spzl-fc-with-gary-aspden/ Look at the stuff Newcastle are getting, read the Gary Aspden quote, then the FF minutes & try not to scream…🤦♂️

-

https://www.thebusinessdesk.com/northwest/news/2166450-kit-supplier-macron-goes-legal-in-dispute-with-blackburn-rovers

-

Hardmen of Ewood Park

Herbie6590 replied to Tim Southampton Rover's topic in Blackburn Rovers Fans Messageboard

He’s been mentioned higher up but John NcNamee probably the hardest I’ve ever seen in Rovers colours.

-

This is referencing Indian residents (not corporations) & overseas income…not losses. DTA are about making sure that individuals aren’t taxed on the same dividend income twice. That doesn’t apply to Rovers - there are no profits therefore no dividends. Corporation Tax is totally different. Whether the loss emanating from an overseas subsidiary can be deducted from Indian consolidated profits is a matter for Indian Corporation tax law. I’m pretty sure this has been debated at length historically on here with the conclusion being that losses CANNOT be offset…thus adding to the mystery of why they own us…

-

I once proclaimed that tax offsetting was possible on here & I was quickly corrected by Harry Berry…supported by a specific document

-

Valérien Ismaël: Former Head Coach

Herbie6590 replied to DE.'s topic in Blackburn Rovers Fans Messageboard

I’m sorry but this post makes absolutely no sense. Please feel to expand upon why relegating an English football club will make a global bank decide to write off loans in a different country secured on assets in that different country. Also, please explain the legal mechanics of how V’s will then go straight to liquidation (bankruptcy is for individuals not companies BTW) without bothering to go into administration & why/how that is beneficial for them? It’s really simple IMO…V’s have reduced the budget (probably at the suggestion of Suhail) & as wage bill & league position are closely correlated in football, the inevitable result ultimately will be relegation.- 5282 replies

-

- 13

-

-

2025-26 Relegation thread

Herbie6590 replied to BRFC4EVA's topic in Blackburn Rovers Fans Messageboard

Ismael signed up for the project. If they change him then Suhail & Rudy have to indoctrinate a new guy…too much like hard work that, so keep the current guy. -

The January 2026 Transfer Window

Herbie6590 replied to chaddyrovers's topic in Blackburn Rovers Fans Messageboard

I’ve heard it said on a number of podcasts that loan deals are often structured around the fee being determined by appearances made - so more games, lower loan fee paid. Rovers will no doubt be balancing that given the urge to cut costs everywhere… -

Revenge for the FA Cup? McLoughlin to score the winner? Mauled by the Tigers? Two wins in 15? Which is it to be? 🤔

-

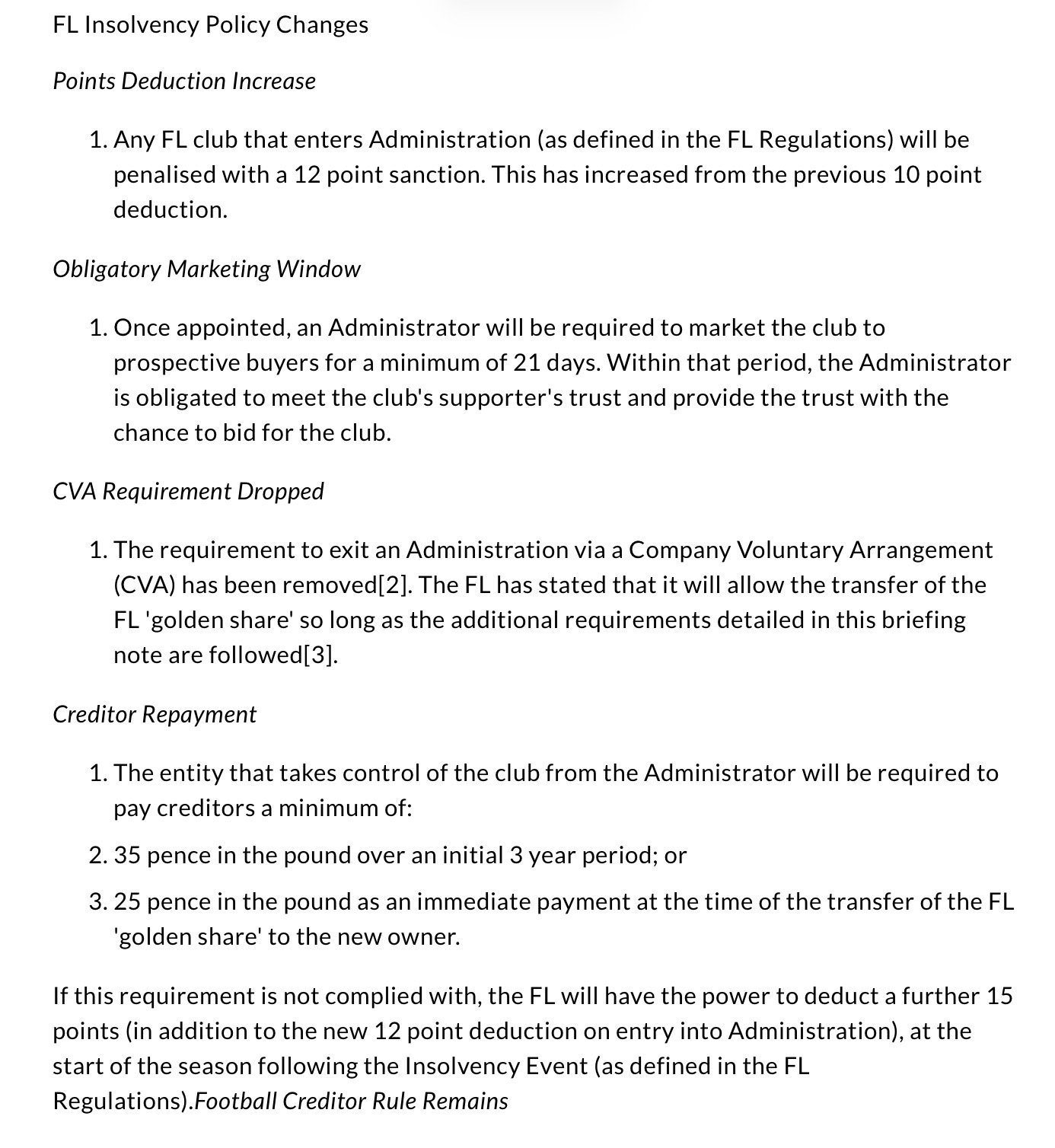

This rule is aimed at new owners. The more they pay to the unsecured creditors of the club, this reduces the chance of a further points deduction. A new owner may of course think “F*ck that…” & swallow the additional points deduction to protect their cash reserves. https://www.danielgeey.com/done-deal-blog/football-league-insolvency-regulation-changes-a-brief-summary

-

They’re bored of their hobby & have set a ceiling on spending.

-

Chansiri says “Hi!” 😉

-

Technical point - but we only end up in Admin if Venky’s decide not to sell, not to fund & the UK directors of the club fear personal liability under insolvency law & to avoid the risk, they therefore call in the administrators. That’s why the departure of SW & a lack of CEO is intriguing. Who would actually do this? Suhail can’t if he isn’t a director. That would be perverse in the extreme, it would mean Venky’s would rather get nothing for the club than even a token bid of £1. I think we can rule out administration for now.

-

v Watford (h) - 24/1/26

Herbie6590 replied to WacoRover's topic in Blackburn Rovers Fans Messageboard

The BRFCS Player of the Match in association with SUITS ME - the official Rovers debit card provider - is ADAM FORSHAW...⚪🔵 MOTM template.mp4 -

I’m always happy to debate on here - in hopefully a grown up manner. The last 4000 Holes podcast for instance, I said I’d make the case against the boycott because I thought it was a good intellectual exercise to rehearse how the boycott might be challenged by others with different viewpoints. I’m not remotely bothered by what is posted elsewhere TBH as there’s bugger all I can do about that - but if someone is civil on here & wants a debate I think that’s what this forum is for…& I’m happy to engage at face value 🤷♂️

-

If they own the business then all the money that business generates belongs to the shareholders of that business (net of any tax etc) for them to use as they deem fit. If the shareholders (owners) then elect not to provide additional share capital/directors loans because income (& cash flow) has increased (albeit temporarily) then that is their choice. Ultimately, all the money in Blackburn Rovers Football & Athletic Ltd “belongs” to the shareholders…i.e. ultimately Venky’s.

-

An eloquent post.